When Structural Transitions Become Black Swans

Hidden instability, structural compression, and the migration of market equilibrium zones

Financial markets often describe extreme events as “Black Swans” — rare and unpredictable shocks that emerge without warning.

But what if the event itself is not the anomaly?

What if the anomaly is the hidden structural condition that existed long before the event became visible?

One of the assumptions deeply embedded in modern finance is that markets move through a relatively continuous and statistically stable process. Under this view, extreme events are treated as external disruptions — exceptions to an otherwise normal system.

But markets do not always behave as continuous equilibrium systems.

In the Market DNA framework, markets can transition between different structural zones depending on how imbalance accumulates across time and price.

Most of the time, markets operate near what could be described as a dynamic equilibrium zone — where temporal progression and price behavior remain relatively synchronized.

But equilibrium is not static.

As participants continuously revalue assets through fear, leverage, liquidity shifts, policy reactions, and collective behavior, structural asymmetries begin to accumulate beneath the surface.

At first, these asymmetries may appear invisible.

Volatility may remain low.

Price may appear stable.

The system may even look healthy.

Yet internally, the market may already be drifting away from its prior equilibrium zone.

Certain structural regions become progressively inactive while opposing regions absorb and accumulate asymmetry beneath the surface.

Over time, the market’s equilibrium zone itself migrates.

And under specific conditions, the accumulated imbalance can transition into a structural release.

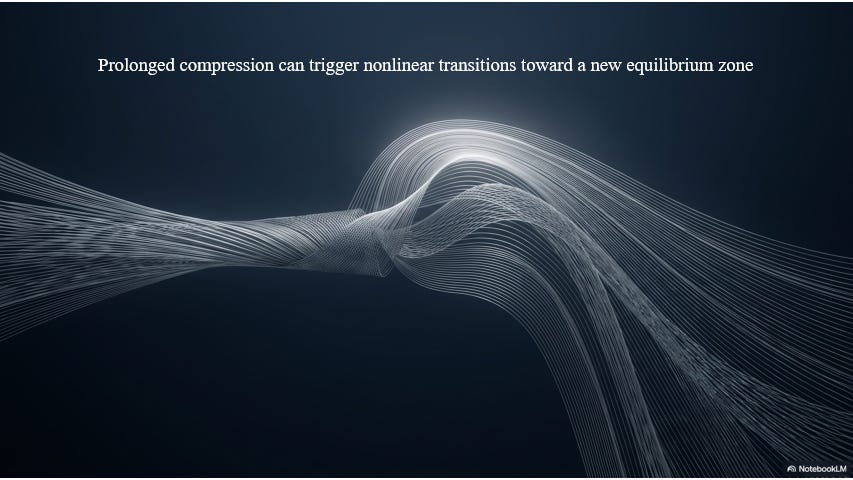

Not every structural transition becomes extreme.

Some transitions occur gradually as imbalance disperses across time.

But when structural pressure remains compressed for prolonged periods, the release can become nonlinear and disproportionately violent.

When this happens, markets do not move incrementally.

They transition between structural zones.

Price no longer reacts step by step.

It attempts to reconnect with a different equilibrium zone altogether.

From the outside, this appears chaotic.

Violent repricing.

Liquidity collapse.

Panic.

Volatility expansion.

What the world later calls a “Black Swan.”

But perhaps the event was never truly random.

Perhaps the instability had already been encoded into the structure long before the release became visible.

The event is not the anomaly.

The market does not become unstable randomly.

Instability emerges when compressed structural asymmetries can no longer remain contained.